Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Should I buy a house now or should I wait for prices/interest rates to go down?

TLDR: If you can afford a 3% down payment and can afford the mortgage payment, you should buy a house now. But don’t take my word for it, I’m a real estate agent who makes money buying and selling houses. The good news is that you don’t have to. You can look at the numbers and see for yourself by reading on. All of the information is here is backed up by industry leaders and source links.

If you’re thinking about buying a home in Portland (or anywhere in today’s market), you’ve probably asked the same question most buyers are asking right now:

Should I wait for prices or interest rates to come down?

On the surface, waiting feels safe. But when you break down the numbers, rent paid over time vs mortgage payments + appreciation, the cost of waiting becomes much clearer.

In many cases, waiting doesn’t just delay buying…

It quietly costs tens of thousands of dollars in lost equity and rising home prices.

Rent vs Buy: The Real Monthly Wealth Difference

Let’s look at a simplified example:

- Average rent: $2,000/month

- Comparable mortgage payment: $2,500/month ($400K home)

- Home appreciation: ~3% annually (historical average)

- Down payment: 3%

What actually happens over 5 years:

| Category | Renting | Buying |

| Monthly payments | $120,000 | $150,000 |

| Equity built | $0 | ~$60,000–$90,000 |

| Home appreciation benefit | $0 | ~$45,000–$75,000 |

| Net wealth position | ❌ -$120K spent | ✅ +$105K-$165K |

Even though buying costs more monthly at first, a large portion is converted into equity and appreciation, not lost forever.

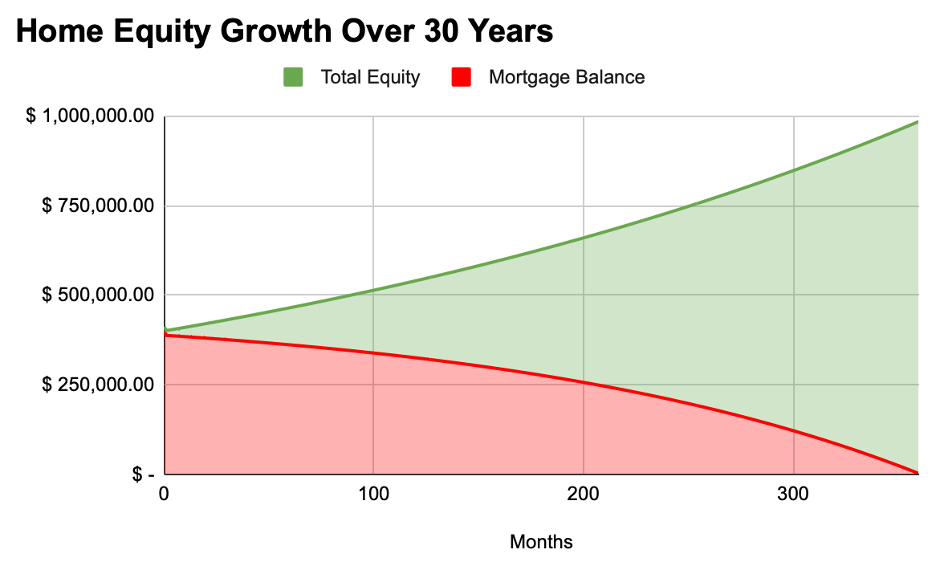

Note: The green area represents the cash that you would expect to get back if you sold your home after the given number of months and rises as home prices increase. The graph is based on a $400K purchase price with a 3% down payment, a 6% interest rate, and 3% annual appreciation, on a 30 year loan.

The Hidden Cost of Waiting 12–24 Months

Waiting sounds harmless… until you look at what typically changes:

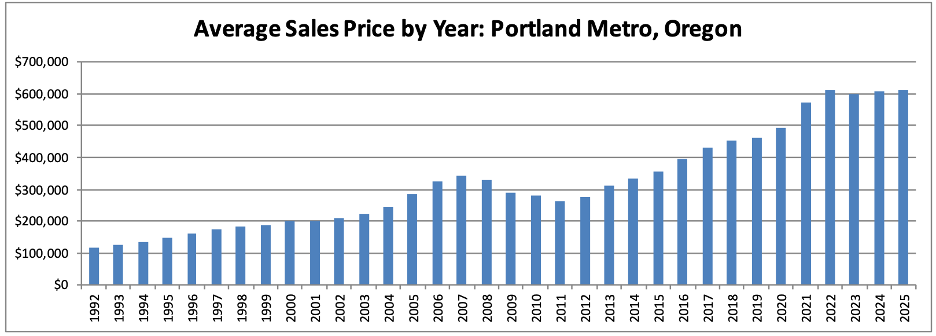

- Home prices keep rising over time

Source: Oregon Regional Multiple Listing Service (RMLS)

Even in “cooling” markets, homes generally trend upward long-term.

At just 3% annual appreciation, a $400,000 home becomes:

- Year 1: $400,000

- Year 3: ~$437,000

- Year 5: ~$464,000

Waiting often means the exact same home costs $30K–$80K more later

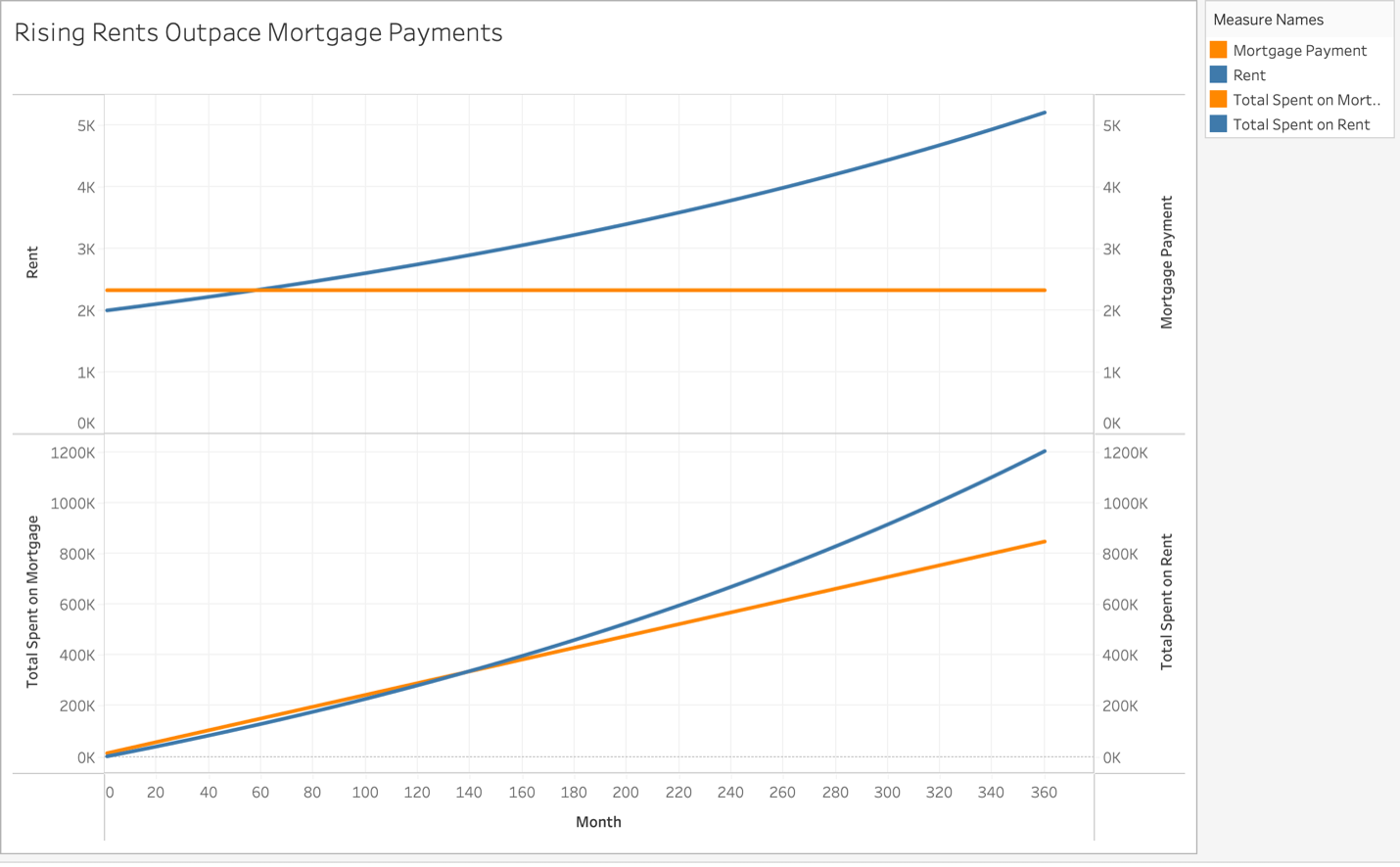

- Rent is 100% spent and equal to a 100% interest rate

Rent does one thing very efficiently: It covers housing, but builds zero ownership

Over 5 years:

- $2,000 rent=$120,000 spent

- No equity

- No appreciation benefit

- No ownership asset

A mortgage works differently than rent:

- Early payments = mostly interest

- Over time = more principal (ownership)

- Home value increases = wealth growth

So even if the monthly costs are a little higher, part of every payment becomes your net worth.

The Real Cost of Waiting (Simple Example)

Let’s say you wait 2 years:

What happens during that time?

- Rent paid: $48,000

- Home price increase: +6%–10%

- Lost equity from not owning: $20K–$60K+

Total opportunity cost of waiting: $60,000–$100,000+ in many markets

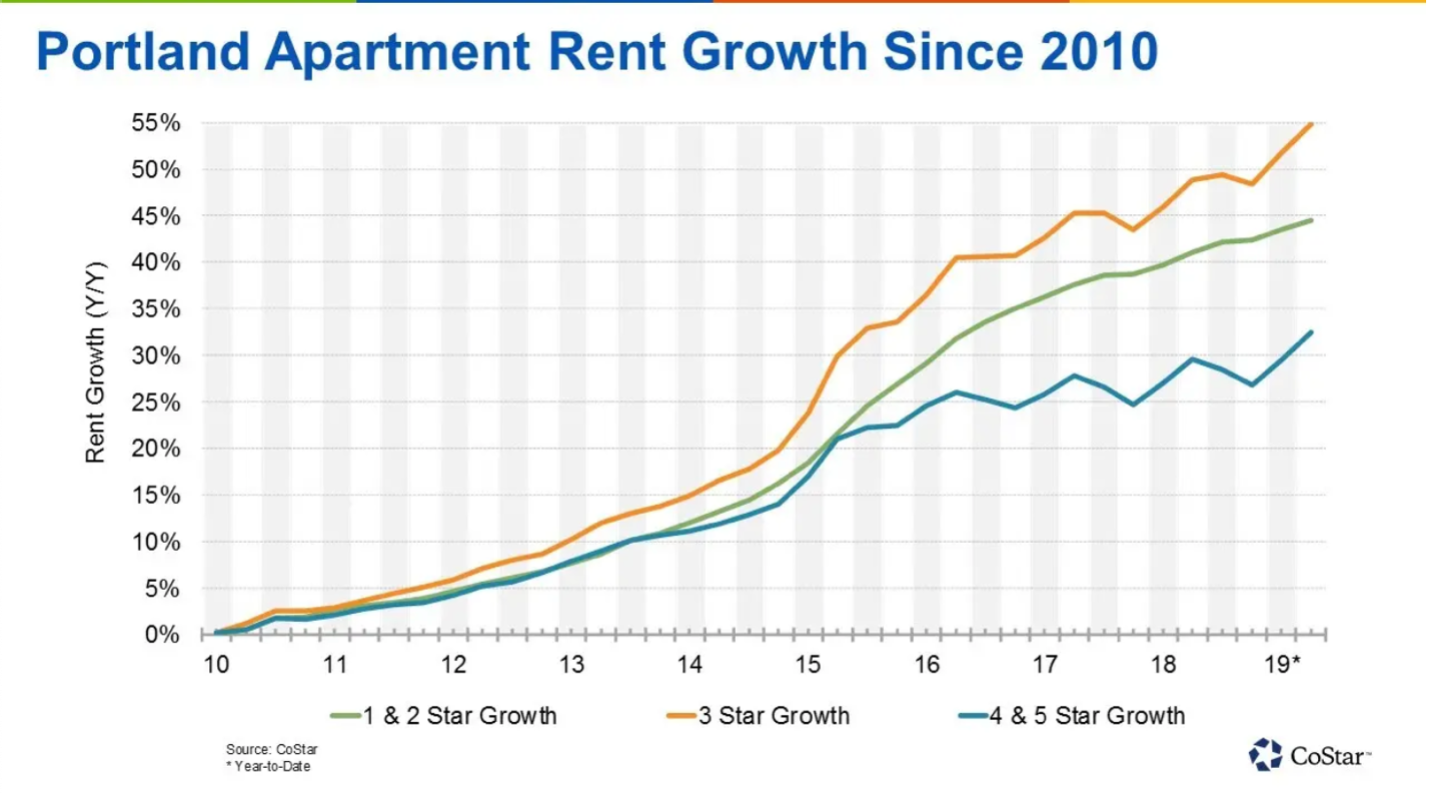

And that’s before factoring in rising rents or tighter inventory, with rents rising an average of 4% per year.

Note: Graph acquired from CoStar, global leader in commercial real estate data.

Conventional mortgage payments don’t change.

🧠 Why most buyers miscalculate timing

People often think:

❌ “Rates will drop, so I’ll save money later”

But they miss:

- Prices are likely rising while you wait

- Competition increases when interest rates fall

- You lose months/years of equity building

- Rent continues with no return on investment

What this means for Portland buyers

In markets like Portland:

- Inventory is limited in desirable neighborhoods

- Good homes still move quickly when priced right

- Rent continues to rise in most areas over time

- Entry prices rarely “crash,” they stabilize or slowly climb

The smarter way to think about timing

Instead of asking: “Should I wait for the perfect time?”

Ask: “How much is waiting costing me in rent + appreciation loss + loan principle?”

In real estate, timing the “perfect market” is extremely difficult, but time in the market is what builds wealth.

Final takeaway

Waiting feels like a strategy.

But financially, it often behaves like this:

❌ Pay rent with no return

❌ Watch home prices rise

❌ Lose months of equity building

❌ Enter the market at a higher cost later

Buying isn’t about timing perfectly; it’s about building equity sooner. Owning a home is the primary investment mechanism for building wealth for middle-class Americans.

Want a personalized breakdown?

If you’re curious what this looks like for your situation in Portland, I can show you:

- Rent vs buy comparison for your price range

- Monthly payment breakdown

- Neighborhood-specific appreciation trends

- Homes you could qualify for today